By Enyichukwu Enemanna

Ghana’s government has announced the scrapping of several COVID-19-era taxes imposed as a means to secure funding from the International Monetary Fund (IMF), attributing the decision to the economic impact on citizens.

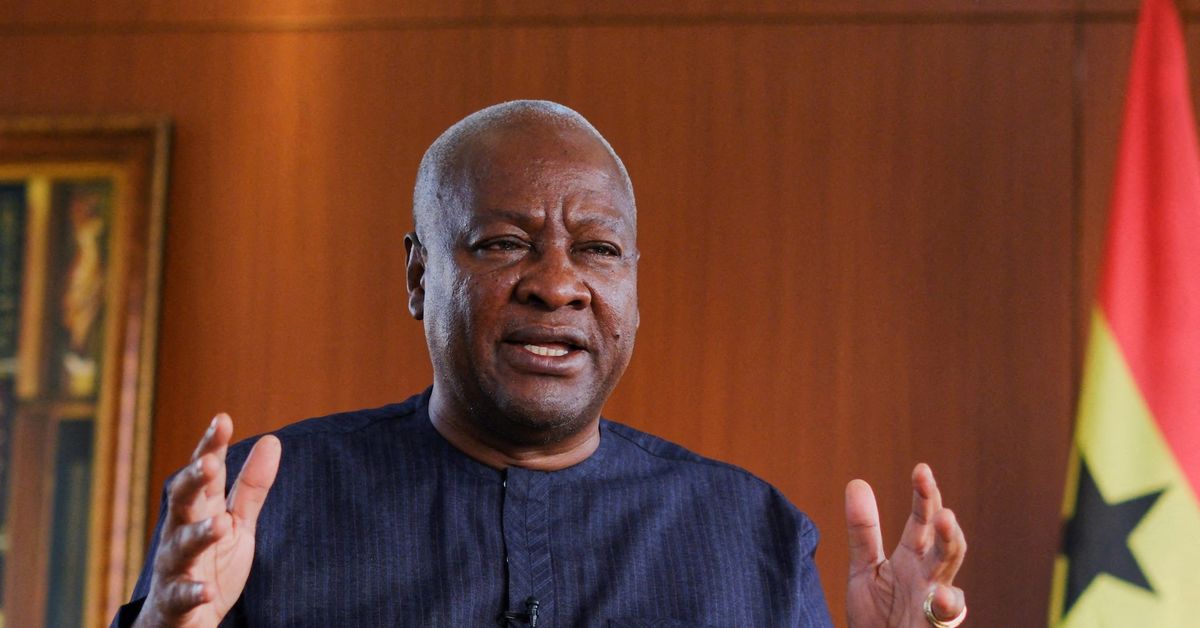

Five different taxes, which President John Dramani Mahama’s administration sees as “nuisance levies,” including a one-percent levy on mobile money transfers and a value-added tax on motor vehicle insurance, are being cancelled, Finance Minister Cassiel Ato Forson announced on Tuesday while presenting the 2025 budget.

With the West African country’s economy in “severe distress,” partly attributable to debt mismanagement and financing shortfalls, analysts have raised concerns over how the government plans to close the resulting revenue shortfall.

The government says it aims to help citizens struggling with soaring inflation and a depreciating currency, seeking to introduce alternative measures to enhance tax collection.

“The removal of these taxes will ease the burden on households and improve their disposable incomes,” the minister told lawmakers in the capital, Accra. “In addition, it will support business growth.”

Other levies abolished include a 10% tax on lottery winnings, an emission levy on industries and vehicles, and a 1.5% tax on unprocessed gold from small-scale miners.

They were introduced as part of efforts by the previous government to reach a $3-billion IMF bailout, which was secured in 2023.

Forson assured parliament that the Mahama government, elected in December but taking office in January, had “stopped the bleeding.”

Plans are in place to amend the Revenue Administration Act to improve tax revenue collection, which is expected to yield an additional 0.3% of GDP, the government stated.

Authorities also aim to improve revenue from road toll collection this year as part of its infrastructure development initiative, which has been dubbed the “Big Push.”

“We inherited an economy in deep crisis, hard hit with debt and beset by other fiscal challenges such as large accumulation of arrears, energy sector financing shortfalls, and large fiscal risks from the cocoa and financial sectors,” Forson said.

In an effort to rebuild the economy, the government is setting up the Ghana Gold Board to help regulate and manage the sector, hoping to increase foreign exchange reserves and stabilise the local currency.

{kind=link}