By John Ikani

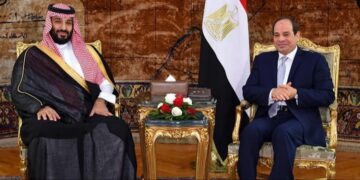

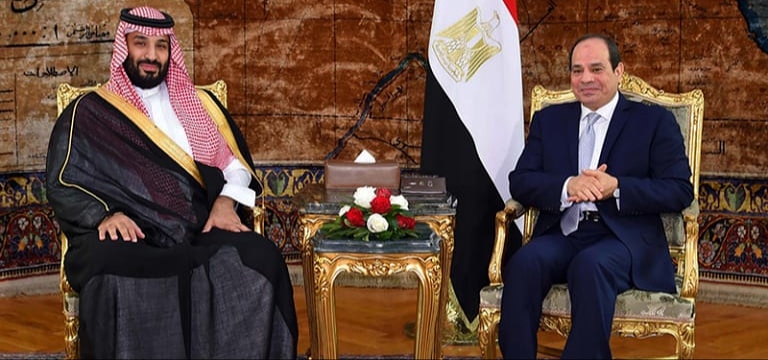

Saudi Arabia has deposited $5bn in Egypt’s central bank in an effort to shore up the economy of the most-populous Arab state, which has come under intense pressure as a result of the Russia’s invasion of Ukraine.

Disclosing this on Wednesday, the state-run Saudi Press Agency (SPA) said the $5bn deposit in the central bank was a part of “tireless efforts” to support Egypt.

Cairo announced last week it was seeking IMF support after the war sent the prices of wheat, cooking oil and fuel soaring and cut the flow of tourists from Russia and Ukraine — both important markets for its crucial tourism sector.

A major food importer, Egypt has been hit hard by record grain prices fueled by Russia’s invasion of Ukraine. One of the Middle East’s most indebted nations, it buys most of its wheat from the two countries currently at war, while Russian visitors previously made up a significant portion of its tourism market.

Egypt is one of the IMF’s biggest borrowers after Argentina and analysts said the country, which had resorted to the fund twice in the last six years, had exceeded its quota of IMF borrowing rights and would probably be required by the lender to secure co-financing from other sources. The deposit from Saudi Arabia would help meet this condition.

Saudi Arabia’s Public Investment Fund is also looking into $10 billion of potential investments in Egypt’s healthcare, education, agriculture and financial sectors, according to an Egyptian cabinet statement.

Egypt will take quick steps to ease the process in order to secure investments expected to come through cooperation between the PIF and Egypt’s sovereign wealth fund, the cabinet statement said.

Asides Saudi Arabia, Qatar on Tuesday pledged to pump $5 billion into investments in Egypt, while Abu Dhabi wealth fund ADQ earlier this month made a roughly $2 billion deal to buy Egyptian state-owned stakes in publicly listed companies.

Some of the assistance reflects a political focus as much as an economic one. Oil-rich Saudi Arabia and the United Arab Emirates pumped in billions of dollars in aid, deposits and investments in recent years.

That aid bolstered Egypt’s economy in the wake of the 2013 ouster of Mohamed Mursi, who hailed from the Muslim Brotherhood, an Islamist political organization many Gulf nations see as a threat.

{kind=link}